Interest rates may be important, but that doesn’t make them easy to measure.

Interest rates have long been a concern for policymakers and

households alike. Indian States began regulating the interest rates charged by

moneylenders as early as the 1940 Bengal Moneylenders Act, which placed strict

upper limits on the interest rates that lenders could charge.[1]

Interest rates are also limited for more formal lenders; the Reserve Bank of

India may have removed the cap of 26% interest rates on microfinance loans, but

MFIs are still regulated in what they are allowed to charge.[2]

Regulations regarding interest rates come out of concerns

that households are being taken advantage of by lenders. Without caps on the

market, households may be too desperate - or may not understand finances well

enough - and ultimately pay a steep price for funds. Conversely, lenders argue

that particularly in areas where lending is risky, the cost of doing business

is so high that capping interest rates prevents them from transacting at all.

The complexity of interest rates makes them particularly

difficult to understand, particularly from a household’s perspective;

converting from a declining balance interest rate to a simple interest rate is

a complex affair, involving the precise number of payments. Interest rates for

loans of different lengths are also not directly comparable without additional

calculations. In practice, it is hard to expect households to know whether a

loan is competitively priced on its face.

As researchers, we also struggle with the question of

understanding interest rates. When studying financial inclusion, accurately

capturing interest rates is of paramount importance, but also uniquely

difficult. In rural India, households borrow not only from formal banks, cooperative

banks or microfinance institutions, which tend to have rigidly structured

loans, but from self-help groups, moneylenders, pawn brokers, and even friends

and neighbors, whose loans tend to be much less structured, and much less

formal. Researchers are tasked with not only finding ways to compare these

interest rates, but with doing so by gathering information from households,

who, although they tend to have an excellent sense of their own financial

situation, may not be able to describe their interest rates in technical terms.

Interest Rates in the

Field: Piloting in Tamil Nadu

Last spring, in the context of a broader study on financial

inclusion in rural Tamil Nadu, we piloted and compared three different ways of

capturing interest rates in a household survey, to try and understand what

sorts of questions would elicit the most accurate responses from households.

The first two

methods of calculating the interest rate followed the same approximate pattern -

first, calculate the total amount which will be repaid over the life cycle of

loan, then calculate the percent difference between that and the principle

amount. The goal is to estimate the interest rate without asking highly

technical questions or constructing complex interest rate equivalences.

In the first method,

the household is asked directly about the total amount they repay; in the

second method, the amount is constructed based on the household’s answers to

questions about the loan structure and their payments. The third method instead

asks for a direct measure of the interest rate, i.e. “On Rs. 100 borrowed, what

is the amount of interest you have to pay?” Although this method is not

sophisticated in terms of distinguishing between structures or types of

interests, we use it to treat the self-reported measure of interest as a crude

measure of the actual interest rate.

The pilot was

conducted in a semi-urban area outside of a large city in central Tamil Nadu.

Over the course of several days, 81 households were interviewed, reporting a

total of 234 loans.

Table 1: Loans by Lenders

Lender

|

Number

|

Percent

|

Private Bank

|

6

|

2.6%

|

NGO/MFI

|

58

|

24.8%

|

Nationalized Bank

|

38

|

16.2%

|

Primary

Agricultural Cooperative (PAC)

|

22

|

9.4%

|

Friend/Neighbor/Relative

|

25

|

10.7%

|

Moneylender

|

16

|

6.8%

|

Pawn Broker

|

34

|

14.5%

|

SHG

|

14

|

6.0%

|

ROSCAS

|

4

|

1.7%

|

Non-Banking

Financial Corporation (NBFC)

|

13

|

5.6%

|

Lender Not

Reported

|

4

|

1.7%

|

Total

|

234

|

100.0%

|

Loans from

microfinance institutions were the most common, comprising a quarter of the

total loans reported. Households also reported a substantial proportion of

loans from nationalized banks and pawn brokers, and, decreasingly, from

friends, neighbors and relatives and from primary agricultural cooperatives. Private

bank loans, despite the proximity of this area to a fairly large city, were

relatively uncommon within the sample, as well loans from ROSCAS (rotating

savings and credit associations).

Table 2: Loans by Loan Type

Loan Type

|

Number

|

Percent

|

JLG Loan

|

87

|

37.2%

|

Land Loan

|

13

|

5.6%

|

Jewelry Loan

|

83

|

35.5%

|

Other

|

51

|

21.8%

|

Total

|

234

|

100.0%

|

Joint lending group

loans (the classic MFI or SHG loan) and jewel loans made up over 70% of the

sample. As one would expect, the majority of JLG loans - nearly 90% - were

reported as from microfinance institutions, non-banking financial corporations

or self-help groups. Most of the rest of the loans reported did not require

collateral, although a small percentage of households reported that they were

required to provide land as collateral for their loans.[3]

Following the

conclusion of the pilot, interest rates were calculated for each of the three

methods for each reported loan. We then looked, for example, at whether the

three methods of calculation agreed for the loan, and how the interest rates

broke down by different lenders and types of loans.

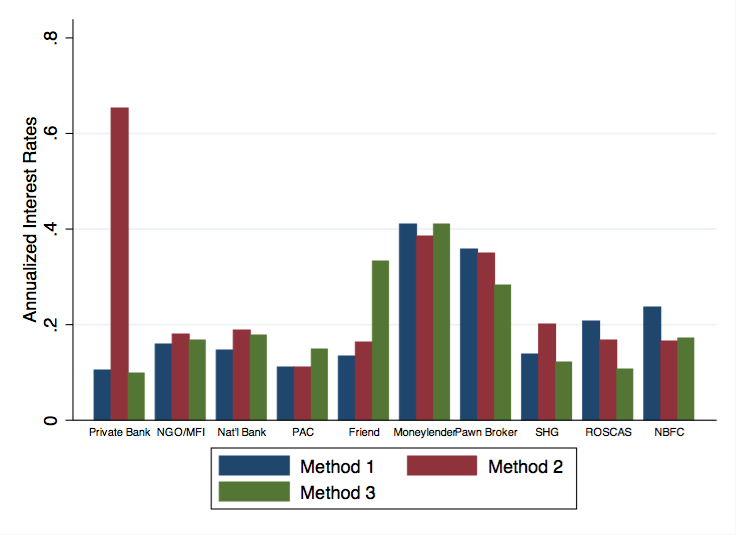

Figure 1: Interest Rates by Lenders

Consistently, across

all three methods, the highest interest rates were reported from loans from

moneylenders and pawn brokers. Correspondingly, although the figure is not

included, joint lending group loans tended to have lower interest rates than

jewelry loans and unsecured loans both. The only exception was the interest

rates calculated via Method 2 (which asks about loan structure, and uses

repayment frequency and repayment size to calculate the total amount which the

respondent will repay) for private bank loans. This - and informal observation

during the survey process - suggests that in the case of formal loans,

respondents often struggle to reproduce precisely their loan schedule, but do

have a good sense, overall, of the cost of the loan and the interest rate which

they are required to pay.

How does

understanding the extent to which self-reported interest rates are accurate and

internally consistent contribute to the broader debate about financial

inclusion in India? Outside of its obvious relevance in research and impact

evaluation, the results of this pilot suggest - tentatively - that, at least

when assisted by surveyors, relatively low-income rural respondents, the majority

of whom had little to no financial literacy training, were relatively

accurately able to report on the interest rates they faced. Respondents could

not necessarily describe their loans in technical terms; they did not necessarily

know precisely their annual percentage rate, or any of the other statistics

used by financial corporations. However, we found that respondents knew what

they would be required to pay back in total, and knew whether a loan was a good

or bad deal. In short, they did have a good sense of how much they were paying

for the money that they had borrowed.

We can’t conclude

from this that interest rates don’t need regulation, and the results of the

pilot don’t address the constraints that households face when there are few

lenders to be found. That being said, the results are encouraging; as financial

inclusion improves in rural India, and as households have the opportunity to

borrow from a wider range of lenders, this pilot suggests they will do so with

a practical, if not technical, understanding of the interest rates they face.

[1] The Bengal Money-Lenders Act, 1940, Chapter VI,

Interest and other charges, p. 16

http://www.wbrsrsa.org/exam_pdf/Bengal%20Money-Lenders%20Act,%201940.pdf

[2]

http://articles.economictimes.indiatimes.com/2014-02-08/news/47127322_1_margin-cap-lending-rate-interest-rate

[3] Households reported being required to provide land as

collateral for a range of loans, from private banks, nationalized banks,

primary agricultural cooperatives, friends, neighbors, relatives and

moneylenders; we remain somewhat skeptical as to the accuracy of this

reporting.

Comments

Post a Comment